If you're retired or getting close to retirement age, making sure your savings last throughout retirement is crucial. In recent years, rising prices (also called inflation) have made this harder by reducing how much your money can buy. Today, costs remain high in areas that matter most to retirees, like healthcare, housing, and daily expenses.

While stocks and bonds can help address this challenge, some retirees prefer to avoid risk. Others worry whether their savings will be enough as living costs increase. For anyone planning for retirement, it's important to understand how rising prices affect your retirement income and how to set up your savings to maintain your buying power.

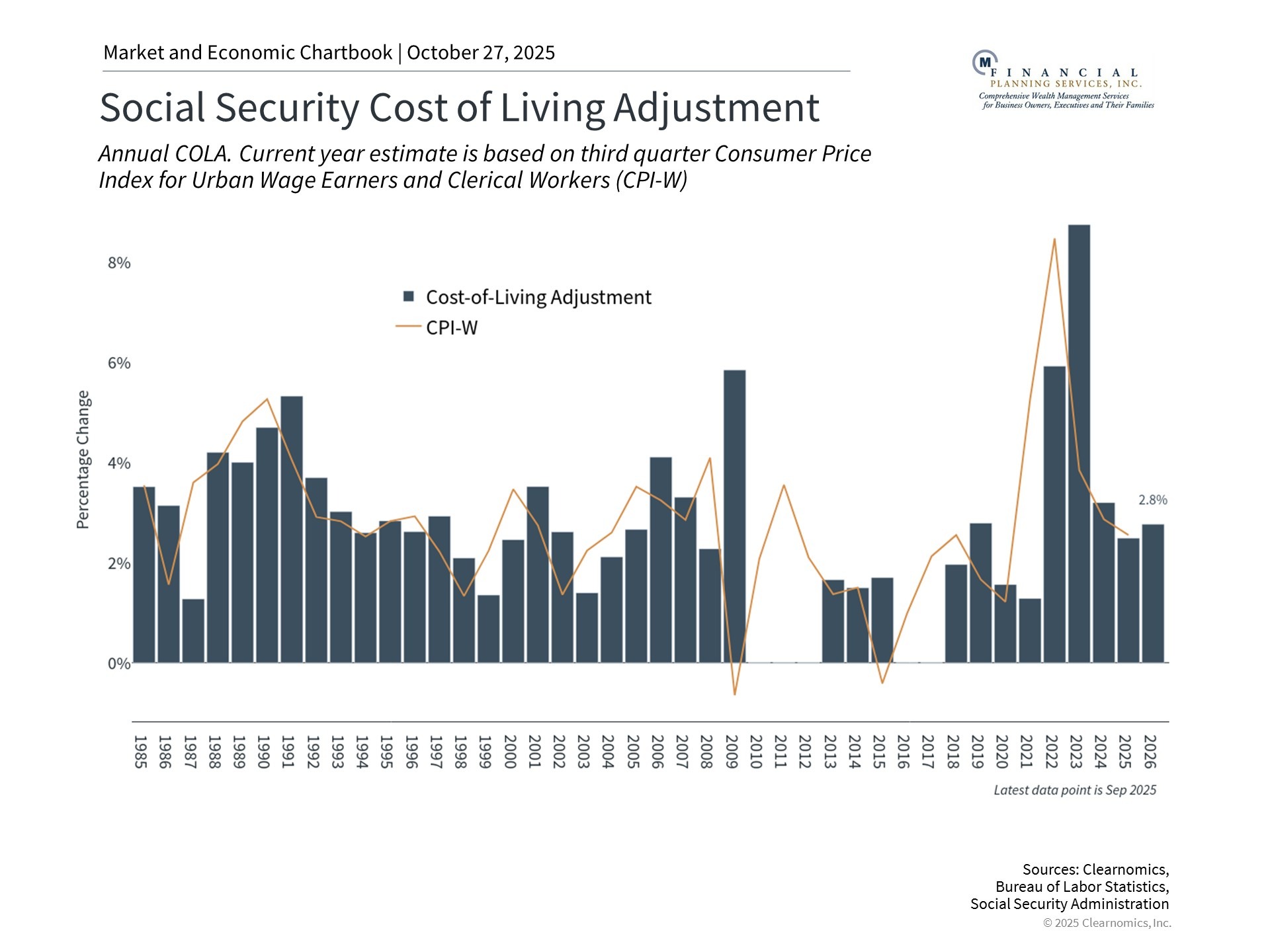

Social Security increases don't always match your actual costs

The Social Security Administration recently announced a 2.8% cost-of-living adjustment (or COLA) for 2026. This means Social Security payments will increase to help keep up with inflation. The average monthly benefit will rise to $2,064, an increase of $56 per month. While helpful, this is much smaller than the 8.7% increase in 2023, which was the largest since 1981.

Here's an important point: even when price increases slow down, prices themselves rarely go back down. The COLA is based on price changes for working households. However, retirees often face different costs than younger workers. Healthcare, housing, and other expenses that retirees spend more on have often increased faster than the overall measure suggests. For example, medical care services rose 3.9% over the past year, while home insurance climbed 7.5%.

Also, Medicare Part B premiums (the amount you pay for Medicare coverage) could rise by $21.50 per month in 2026. Since this is usually taken directly from Social Security checks, it would use up about 38% of the average $56 COLA increase, leaving retirees with less actual purchasing power.

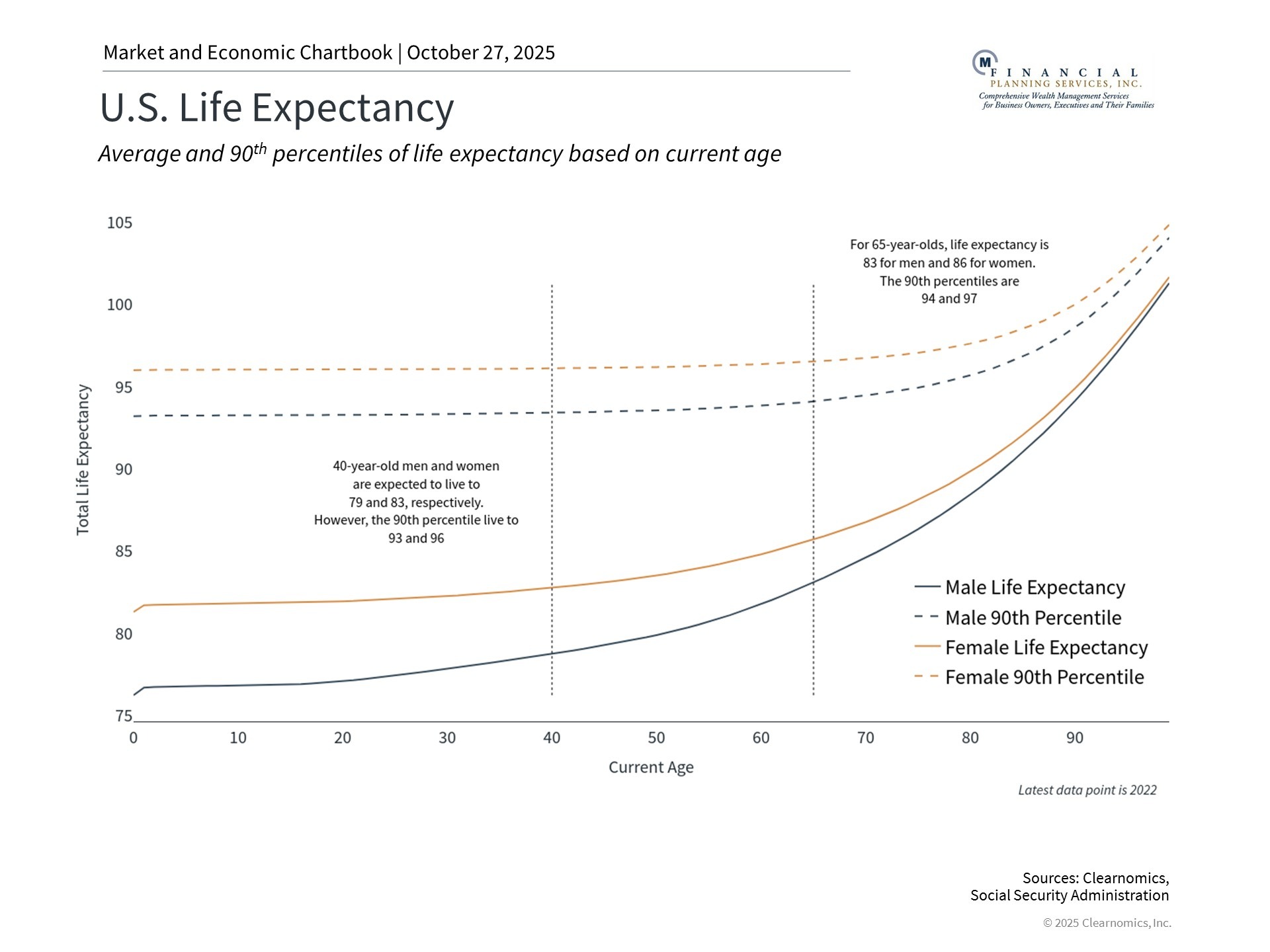

Living longer means your portfolio needs to grow

When your savings don't keep up with inflation, you lose purchasing power over time. This matters even more today because people are living longer than previous generations. According to Social Security data, if you reach age 65, you can expect to live to age 83 if you're male or 86 if you're female on average. Some people live much longer—into their 90s.

While living longer is wonderful, it means your retirement savings need to last longer too. A 30-year retirement requires a different approach than a 20-year retirement. This is sometimes called "longevity risk"—the risk of outliving your money. Many people focus on income from bonds when planning for retirement, but it's also important to include growth investments like stocks, which have historically outpaced inflation over long periods.

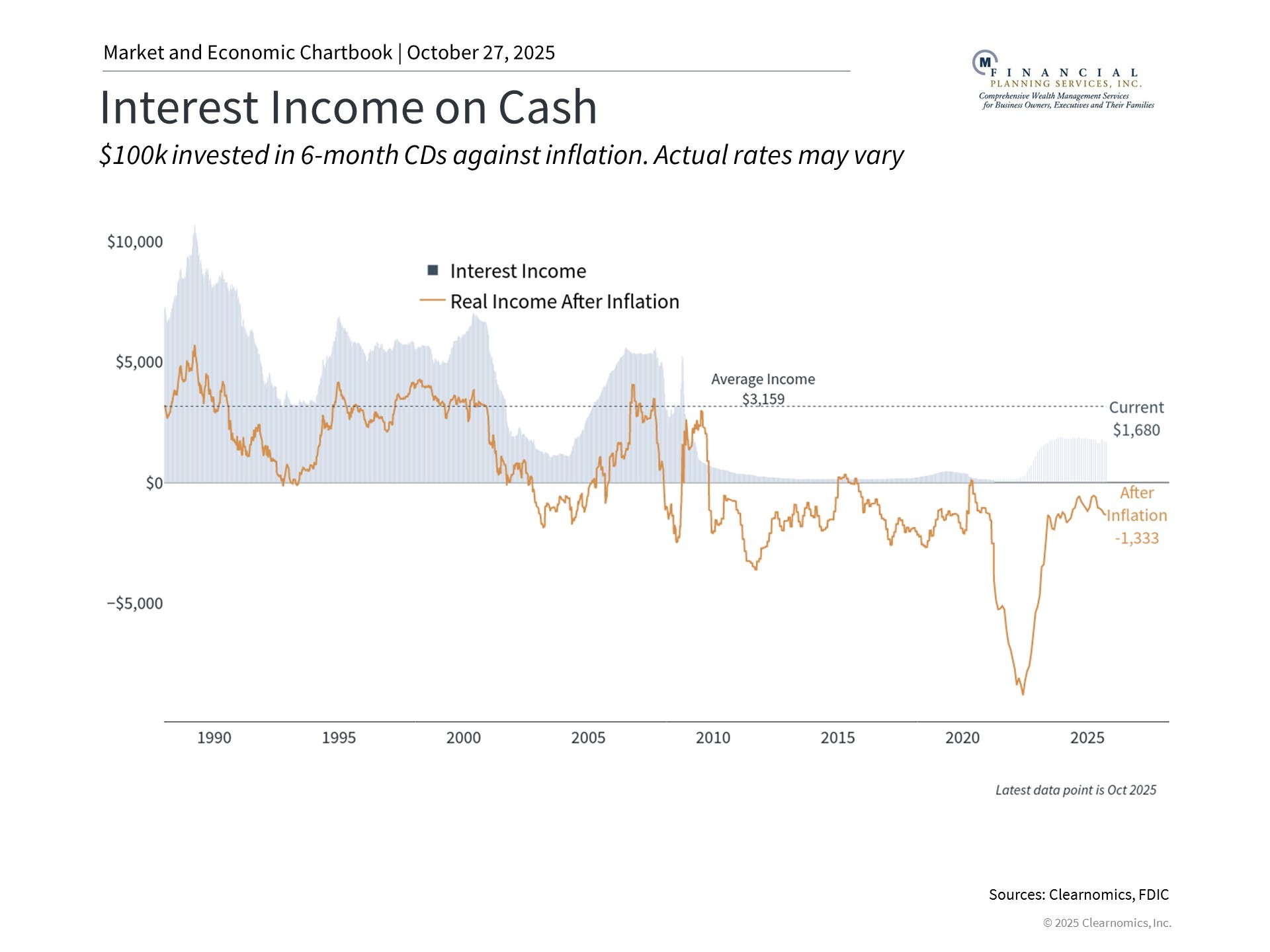

Lower interest rates mean less income from cash

The Federal Reserve (the Fed) is expected to continue gradually lowering interest rates. This is generally positive for the economy, but it means the interest you earn on cash and money market accounts will likely decrease over time. For retirees who have relied on interest income from cash savings in recent years, this shift may present a challenge.

While keeping some cash for near-term expenses and emergencies is important, relying too much on cash means missing out on growth from stocks and income from bonds. The combination of ongoing inflation and declining interest rates makes it harder for conservative investors. Cash loses buying power to inflation, and the interest it generates will decline as rates fall.

The bottom line? Social Security cost-of-living adjustments provide some help, but they're not enough on their own. With people living longer and interest rates declining, retirees need a mix of investments that can provide both income and growth over time.

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.