For much of the history of the stock market, investing was primarily about individual stocks and bonds. Over the past few decades, however, macroeconomic developments have increasingly influenced markets. Significant events, whether related to central bank policy, geopolitics, or global trade, now affect nearly all stocks across the market, regardless of their individual stories. For investors, this means that building modern portfolios is less about finding attractive stocks, and more about making asset allocation decisions that are aligned with financial goals.

This has been the case over the past year and a half, since the two biggest macroeconomic drivers have been the war in Iran and U.S. tariff policy. While these are quite different, they both affect consumer prices and business demand, either directly through higher energy prices or indirectly through the cost of imported goods. A key characteristic of these macro-driven events, however, is that their effects tend to fade over time. Thus, it’s important for investors to stay focused on the longer-term trends, and avoid the temptation to make portfolio changes based on a single event.

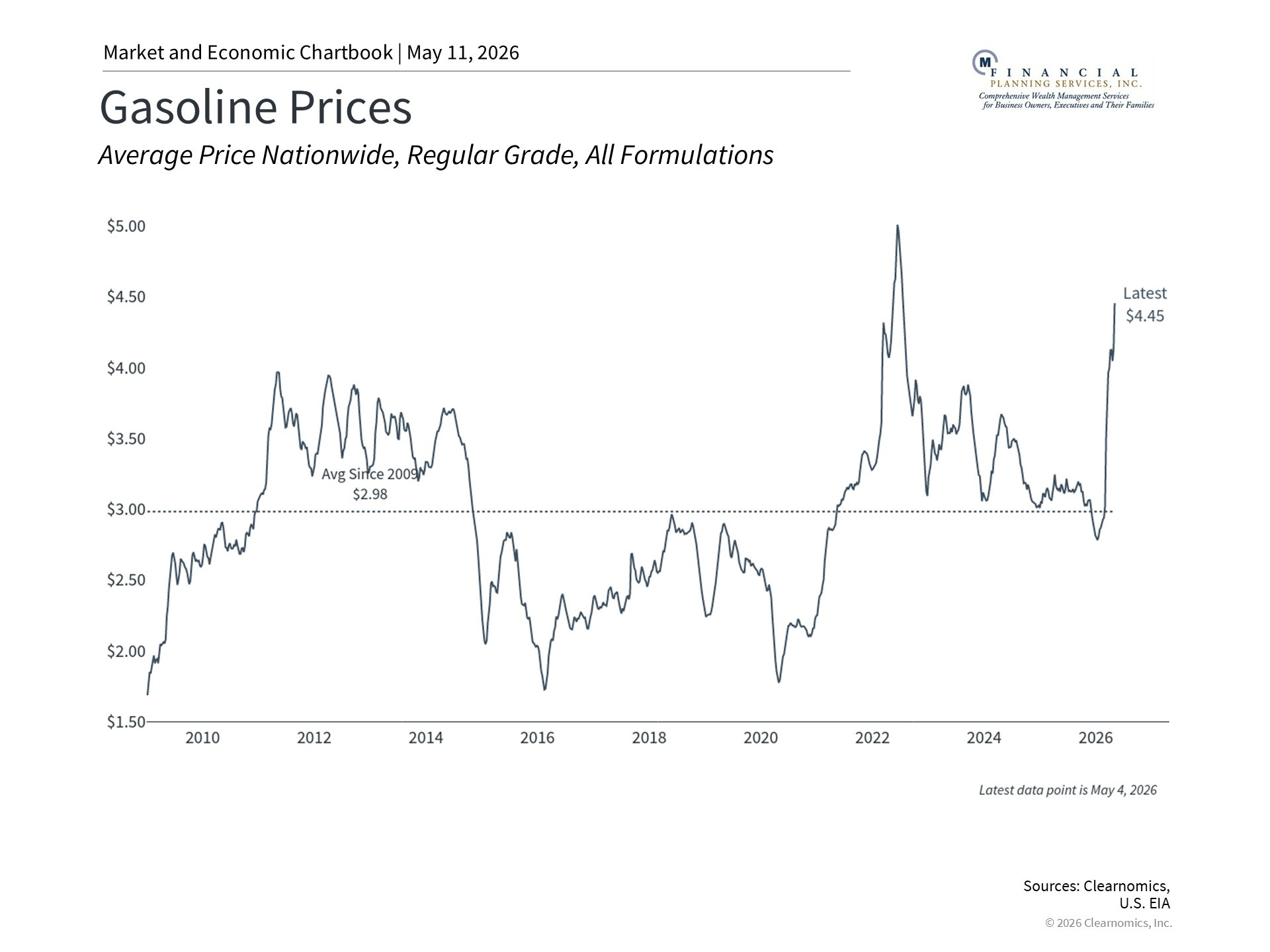

The war in the middle east, gasoline prices, and OPEC

The most visible way the conflict in Iran has reached American households is through the price at the pump. The national average for regular unleaded gasoline has climbed to around $4.50 per gallon, well above the long-term average and a meaningful jump from levels seen just a few months ago. In some parts of the country, gasoline is already above $6 per gallon.1 Because energy expenses directly affect the Consumer Price Index, headline inflation has moved higher, complicating an economic picture that was previously improving.

For some, this environment may bring back memories of the 1970s Arab Oil Embargo, when oil supply shocks led to skyrocketing inflation and gasoline rationing. However, the world has changed considerably since then. First, the U.S. is now the largest energy producer in the world, pumping more than 13 million barrels of oil per day. This has helped to reduce the sensitivity of the U.S. economy to global oil disruptions.

Second, the recent decision by the United Arab Emirates (UAE) to exit OPEC is another reminder of how the global energy landscape has changed. For decades, OPEC members played a central role in setting global oil prices. This was primarily done by agreeing on production levels, which is difficult to achieve and verify across about a dozen countries. Specifically, it is difficult to prevent OPEC member countries from producing more than their agreed-upon limits.

The UAE's departure shows how the cartel is not as relevant as it once was, as member countries pursue their own national strategies and production capacities. At its peak in the 1970s, OPEC accounted for at least half of the world’s oil supply. Today, it is closer to one-third.2 To offset this, a broader group known as OPEC+, which includes Russia and other countries, was formed, but the same coordination challenges apply.

So, the declining relevance of OPEC does not eliminate the risk of oil price spikes during geopolitical events, but it does mean that oil prices are not quite as sensitive to their decisions as in the past. While this provides little comfort to households whose budgets are affected by higher gasoline prices, it does help to explain why the impact on markets has not been more dramatic.

Tariff policy continues to evolve through the courts

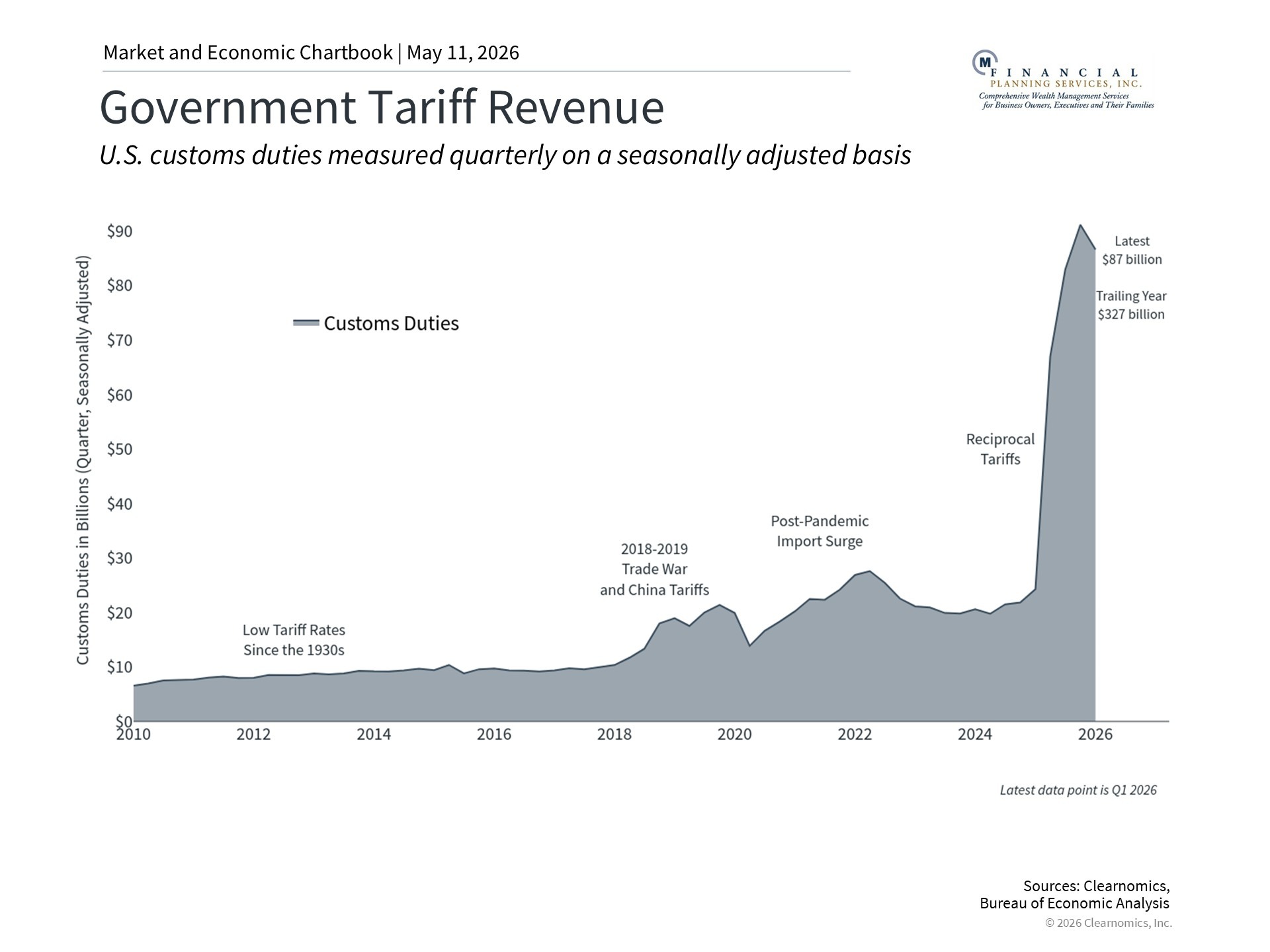

The second major macroeconomic driver has been tariff policy, which continues to face legal challenges. In February, the Supreme Court ruled that the tariffs implemented last April under the International Emergency Economic Powers Act (IEEPA) are illegal.3 In response, the administration shifted these tariffs to utilize what is known as Section 122 of the Trade Act of 1974. More recently, the U.S. Court of International Trade ruled that these Section 122 tariffs are also unlawful.4

On the one hand, the administration will continue to pursue tariffs as a key part of their geopolitical strategy. The administration has other legal authorities it can potentially rely on, including Section 301 of the Trade Act of 1974, which allows for tariffs after investigations into specific countries' trade practices. These investigations have already been launched against dozens of countries, which suggests that tariffs will likely continue, just in the form of country-specific rates.

On the other hand, the refund process for previously collected tariffs is now underway. Customs and Border Protection has begun processing refund claims, and some importers have already started receiving payments.5 Estimates suggest that these could total $160 to $170 billion.

While the total scope and timing of refunds remains uncertain, any that do occur could boost earnings and cash flow for the importers that paid them. From a purely economic perspective, this represents a transfer that was first taken away and is now being returned, so it is not a true gain per se. Regardless, they are positive for businesses and consumers.

Markets have reached new all-time highs despite uncertainty

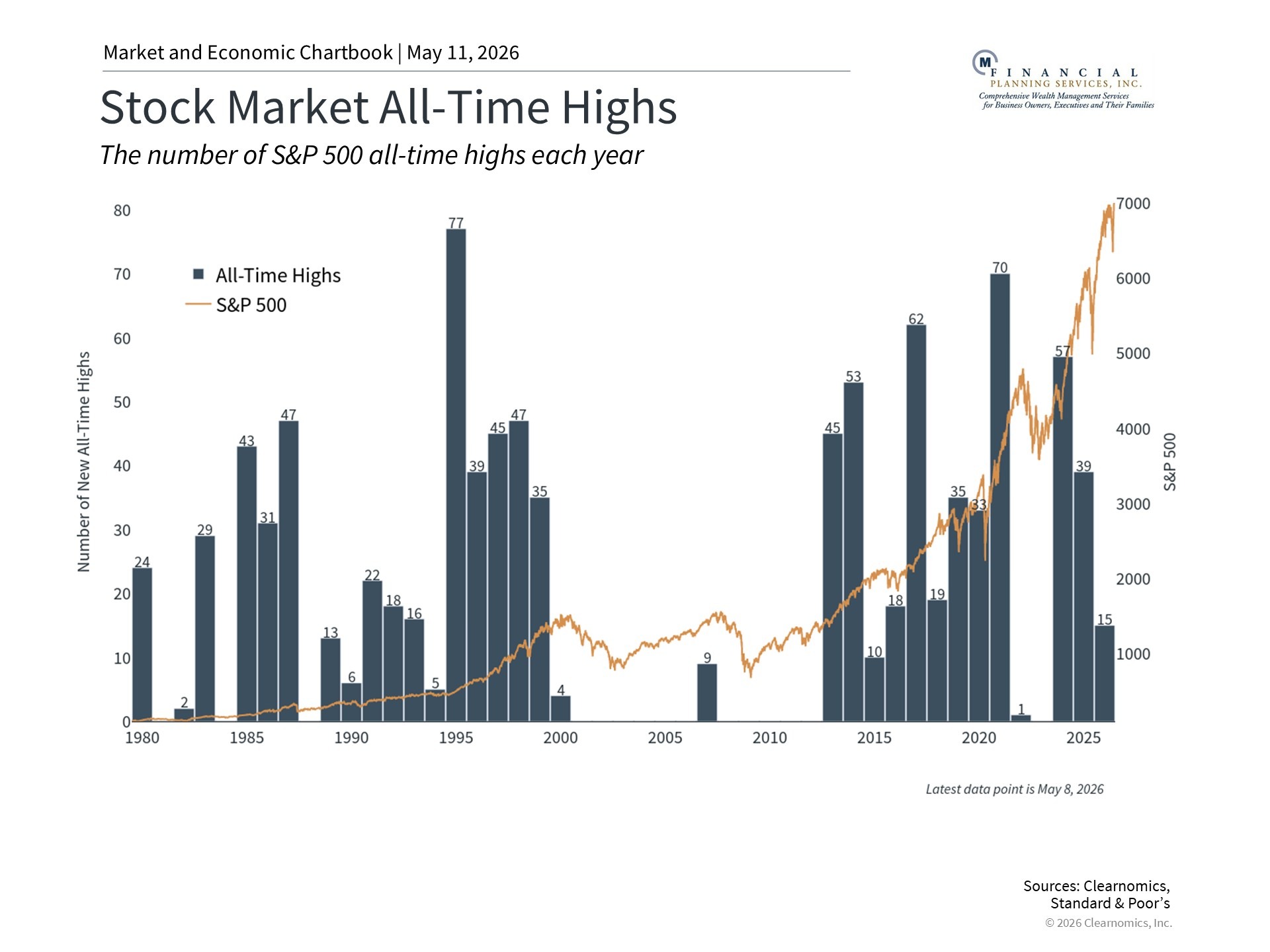

For investors, global events mean that broad market indices and individual stocks can swing based on events that have little to do with any specific company's performance. However, another characteristic of these types of events is that their impact on markets tends to fade over time. Headlines around wars, oil prices, tariffs, and other issues can create volatility, but they are rarely the factors that determine long-term outcomes.

This is why, despite all of the uncertainty of the past year and a half, the S&P 500 has still achieved more than a dozen new all-time highs this year. As the accompanying chart shows, new all-time highs are a normal feature of bull markets, despite the steady stream of investor concerns. What matters is the broader backdrop of corporate earnings and economic growth, all of which have remained healthy.

The bottom line? Today's market environment is shaped by global forces that tend to come and go. Staying invested with a well-constructed portfolio remains the best way to navigate uncertainty and achieve long-term financial goals.

References

1. https://gasprices.aaa.com

2. https://www.eia.gov/international/content/analysis/special_topics/Global_Surplus_Crude_Oil_Production_Capacity/full-report.pdf

3. https://www.congress.gov/crs-product/LSB11398

4. https://www.cit.uscourts.gov/sites/cit/files/26-47.pdf

5. https://www.cbp.gov/trade/programs-administration/trade-remedies/ieepa-duty-refunds

Index Description

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

Securities and advisory services offered through LPL Financial, a registered investment advisor. Member FINRA / SIPC. Financial planning offered through M Financial Planning Services, a Registered Investment Advisor and a separate entity.

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Copyright (c) 2026 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from

sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No

representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the

information and opinions contained herein. The views and the other information provided are subject to change without

notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued

without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and

are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past

performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned

occasionally, but should not be construed as a recommendation to buy, sell, or hold the company's stock. Predictions,

forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any

security--including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text,

images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute

valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be

deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not

limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property,

including without limitation the right to block the transfer of its products and services and/or to track usage thereof,

through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc.

reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil

remedies for the violation of its rights.