Health care costs keep going up year after year. For someone retiring at age 65 today, health expenses could reach about $165,000 throughout retirement – and nearly twice that amount for couples.1 As we live longer, planning for these costs is becoming a crucial part of financial planning.

There are several ways to prepare for future medical expenses, including special tax-advantaged accounts, Medicare supplements, long-term care insurance, and careful retirement income planning. One particularly valuable option is the Health Savings Account (HSA), which offers exceptional tax benefits but remains underused by many eligible people.

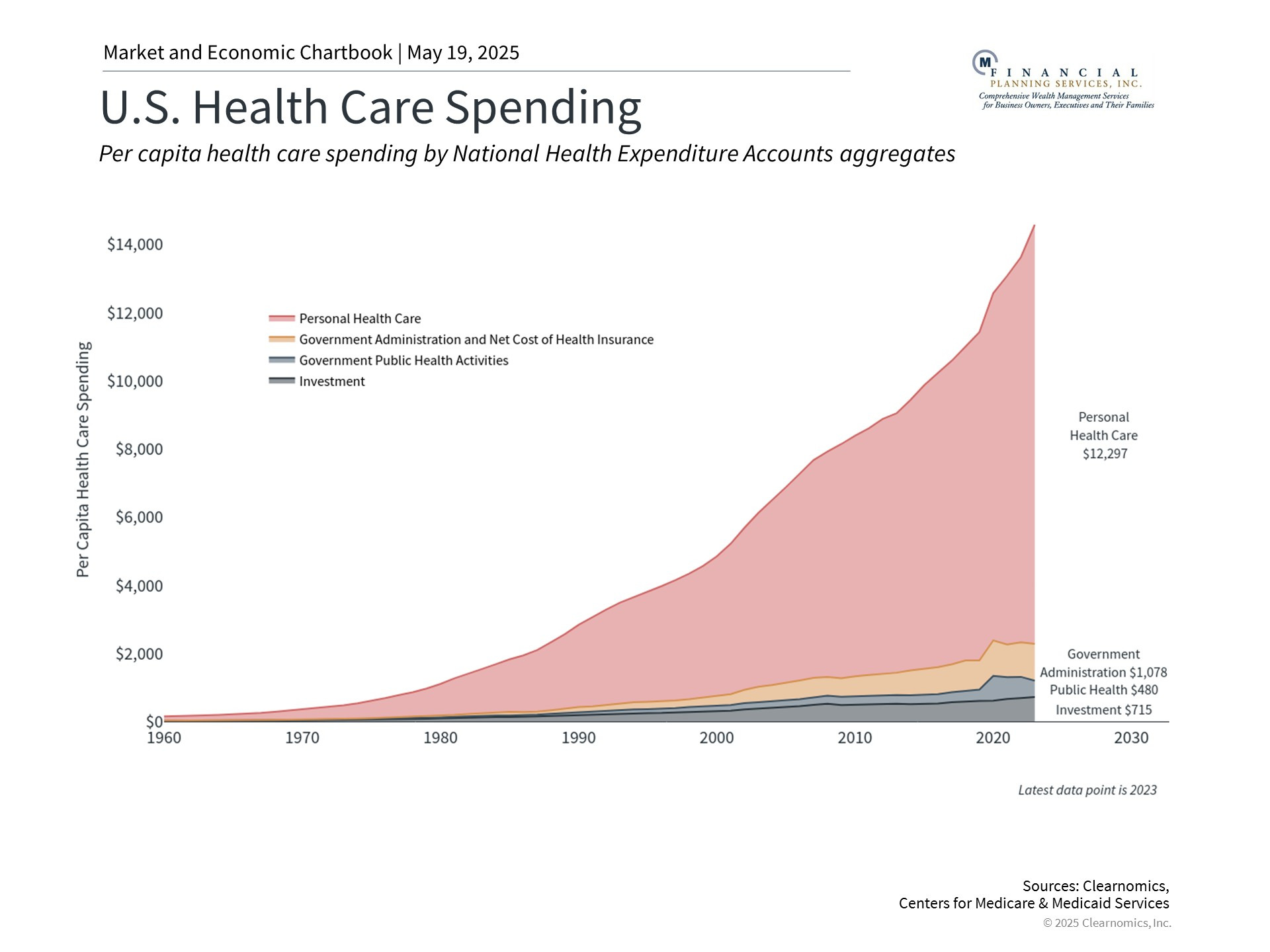

Health care expenses continue to climb each year

In 2023, Americans spent about $4.9 trillion on health care – roughly $12,297 per person and nearly 18% of our country's total economic output.2 This is a huge increase from just 5% in 1962.

When planning for health care costs, consider these three areas:

- Tax planning: Using tax-friendly accounts like HSAs to pay for medical expenses

- Retirement planning: Understanding future health needs and how to fund them

- Estate planning: Deciding what happens to unused health care funds

HSAs offer powerful tax benefits

HSAs are available to people with high-deductible health plans (HDHPs). In 2026, this means plans with minimum deductibles of $1,700 for individuals or $3,400 for families.3

What makes HSAs special is their three major tax advantages:

- Contributions are tax-deductible, reducing your taxable income

- Money in the account grows tax-free

- Withdrawals for qualified medical expenses are completely tax-free

For 2026, you can contribute up to $4,400 annually for individual coverage or $8,750 for family coverage. If you're 55 or older, you can add an extra $1,000 per year.

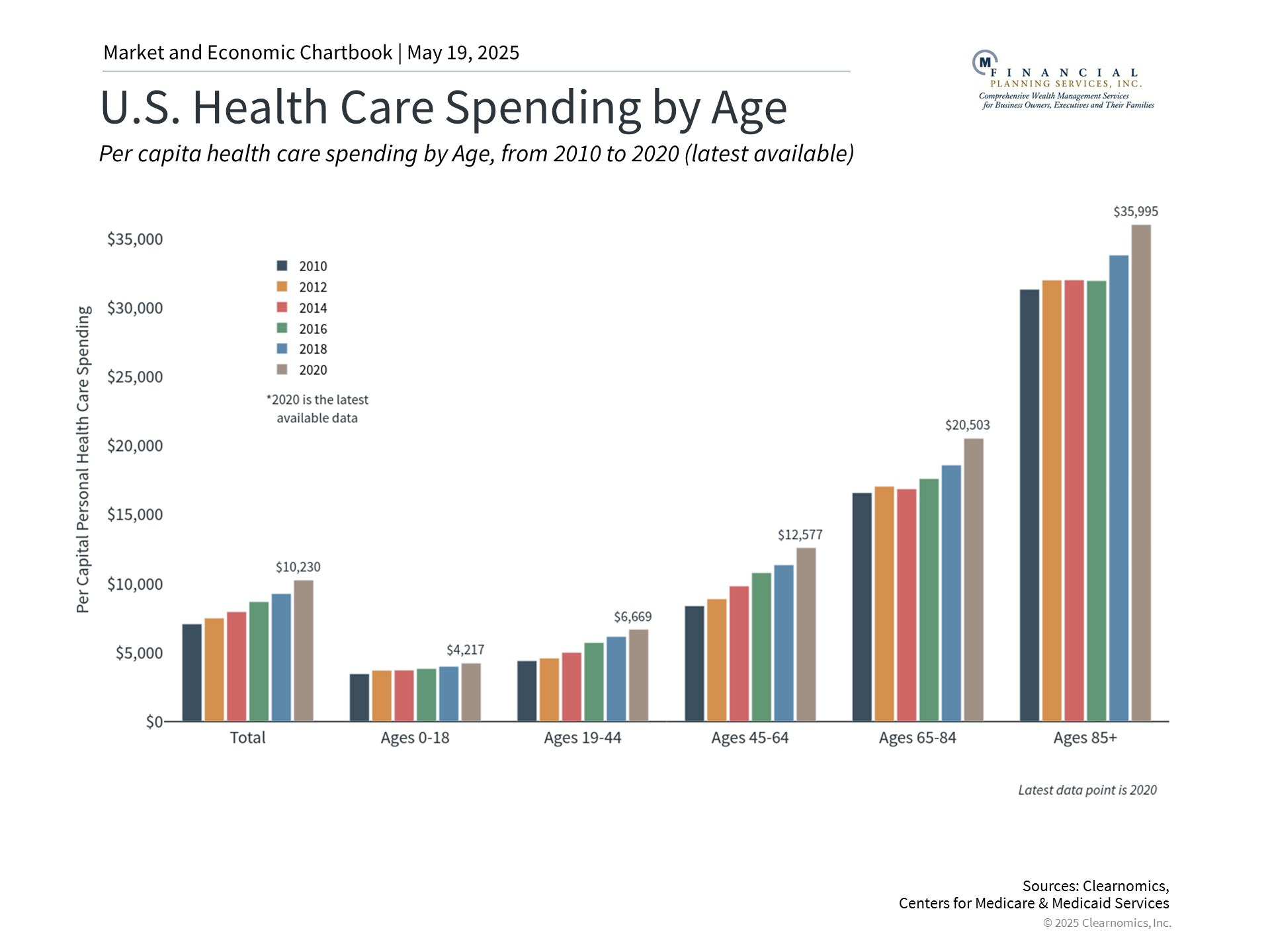

Health care costs are highest in retirement

One smart strategy many people miss is treating your HSA as a long-term investment account specifically for future health expenses. You can maximize contributions while paying current medical costs out-of-pocket, saving receipts for tax-free reimbursements later – even decades later if you choose.

Unlike retirement accounts, HSAs don't require minimum distributions during your lifetime. After age 65, you can even use HSA funds for non-medical expenses without penalty (though regular income tax would apply).

For estate planning, HSAs offer special benefits when your spouse is the beneficiary – they inherit the account with all tax advantages intact. For non-spouse beneficiaries, the tax treatment is less favorable.

The bottom line? Health care will likely be one of your biggest expenses in retirement. HSAs offer unmatched tax benefits to help manage these costs. If you're eligible for an HSA, consider making it a core part of your financial planning strategy.

***

1. https://www.fidelity.com/viewpoints/personal-finance/plan-for-rising-health-care-costs

2. https://www.ama-assn.org/about/ama-research/trends-health-care-spending

3. https://www.irs.gov/government-entities/federal-state-local-governments/where-can-i-learn-more-about-health-savings-accounts-hsa-and-health-reimbursement-arrangements-hra