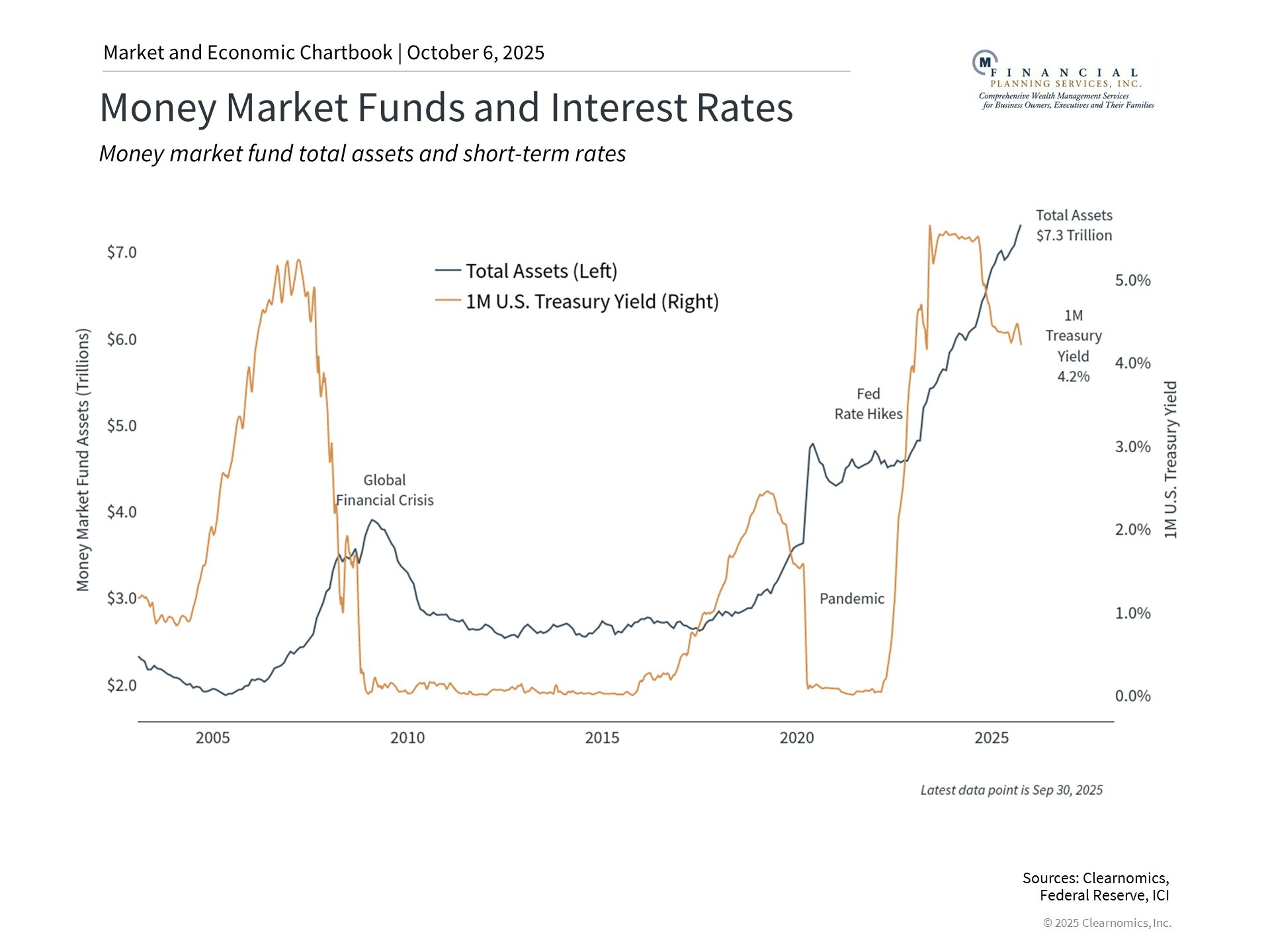

Many investors today face a challenge: what to do with their cash as interest rates decline. While cash might feel like the safest option, keeping too much of it can actually hurt your long-term financial goals. This matters now more than ever, as investors are holding a record $7.3 trillion in money market funds—accounts that hold cash and pay interest.

Successful investing isn't about choosing between risky investments and cash. It's about finding the right balance of different assets that match your financial plans. Cash is important for paying bills and having money set aside for emergencies. But when you hold more cash than you need, you might miss out on opportunities to grow your money and reach your goals.

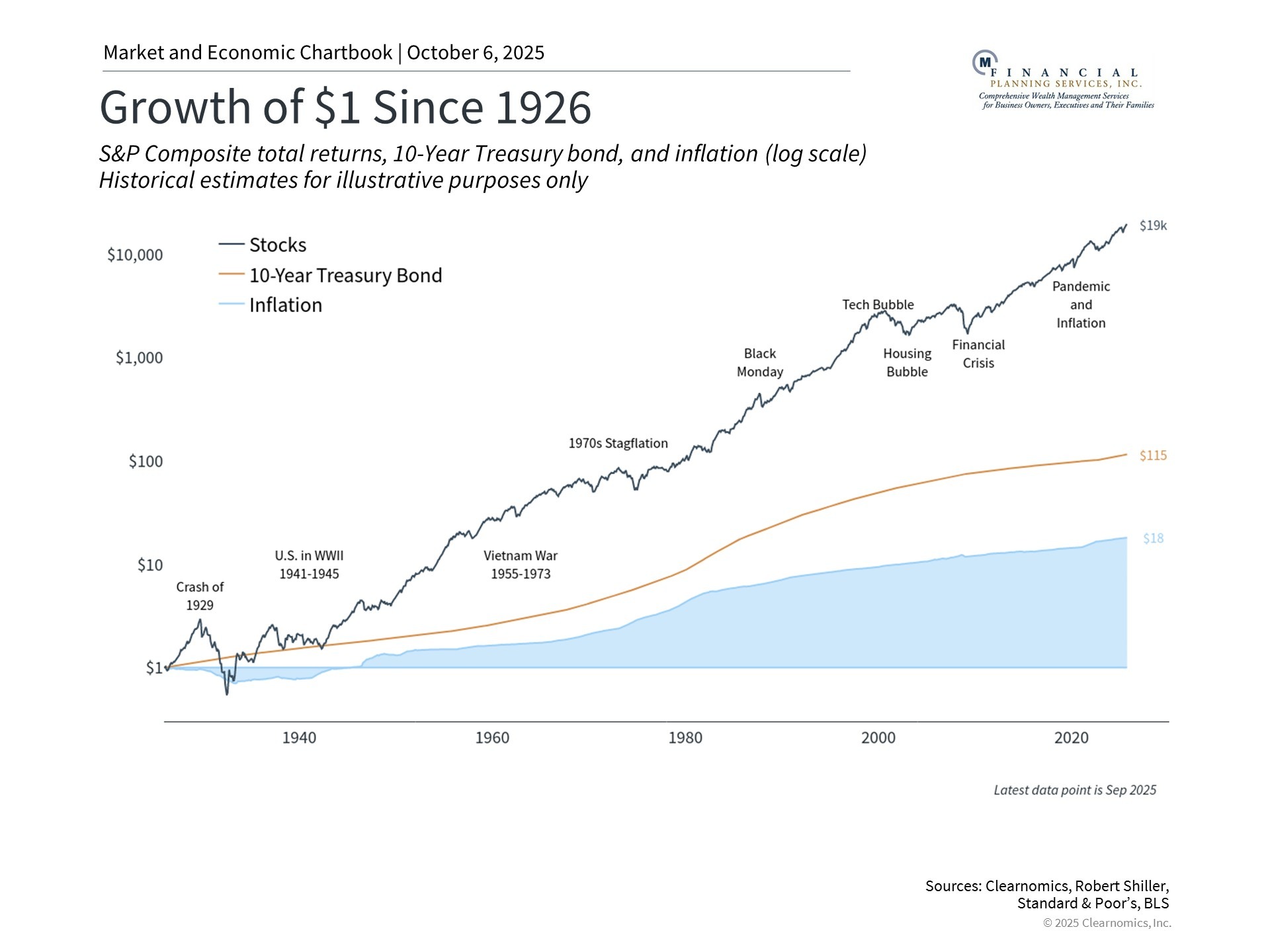

Over time, stocks and bonds have grown faster than inflation

History shows that stocks and bonds have been effective at growing wealth over long periods. The chart above shows that since 1926, stocks and bonds have increased in value much more than the cost of everyday goods (inflation). While $1 in 1926 would buy you what $18 buys today, stocks and bonds grew by much larger amounts. This growth happened despite market downturns, financial crises, and economic recessions along the way.

Cash does serve important purposes in financial planning. You need cash for upcoming expenses and emergencies. For example, if you're planning to buy a house soon or pay tuition next year, keeping that money in cash makes sense. The same goes for emergency savings to cover unexpected costs like medical bills or job loss.

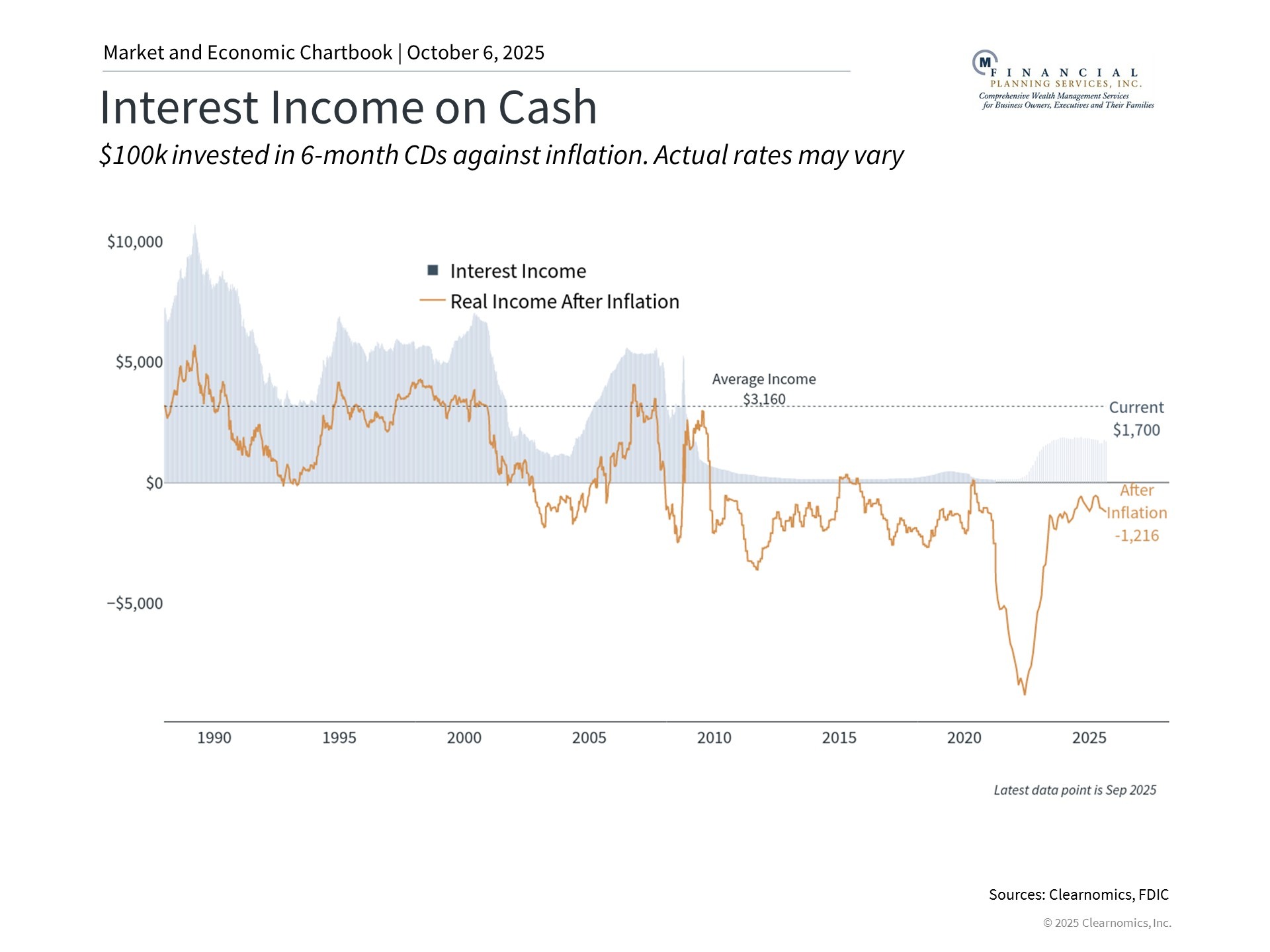

Excess cash loses value over time

Problems arise when you hold more cash than needed for these practical purposes. This has been common recently because of market uncertainty and relatively high interest rates on cash accounts. When cash pays good interest compared to other investments, it can seem like a safe way to earn income. However, there are two hidden costs.

The first hidden cost is inflation—the rising cost of goods and services. Even when savings accounts or money market funds pay decent interest, they often don't keep up with inflation year after year. The chart above shows that after accounting for inflation, cash has actually lost purchasing power during most of the past two decades.

The second hidden cost relates to how cash interest rates work. Interest rates on savings accounts and money market funds can change at any time. While introductory rates might look attractive, these rates aren't guaranteed and typically adjust over time. If the Federal Reserve continues lowering rates as expected, the interest you earn on cash could drop below the inflation rate.

This differs from longer-term bonds, where you can lock in an interest rate for years. For example, if you buy a 10-year Treasury bond today, you secure that interest rate for the full decade, regardless of what happens to rates in the future.

Cash feels safe because your account balance stays steady, even when markets are uncertain. But what matters most is what your money can actually buy, not just the dollar amount in your account. If inflation runs at 3% while your cash earns 2%, you're losing 1% of purchasing power each year. Over decades, this small difference adds up and can significantly impact your retirement and other long-term goals.

Cash holdings have reached record levels

As shown in the chart, money market fund assets have reached $7.3 trillion—nearly double the amount held before the pandemic. This reflects investors seeking higher short-term interest rates and hesitancy about longer-term investments. However, as rates decline, these large cash holdings face challenges. Investors who moved money to cash when rates were high may now face difficult decisions about where to invest next.

The best approach depends on your specific goals. One strategy is dollar-cost averaging, which means gradually moving money from cash into investments over time. This can be helpful now, as bond yields remain attractive compared to history and the stock market has performed well this year.

The bottom line? Cash is important for short-term needs and emergencies. But holding too much cash creates hidden costs through inflation and changing interest rates. For long-term goals, staying invested in a balanced portfolio remains the best approach.

The content is developed from sources believed to be providing accurate information and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

Government bonds and Treasury bills are guaranteed by the US government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value.

CDs are FDIC insured to specific limits and offer a fixed rate of return if held to maturity, whereas investing in securities is subject to market risk including loss of principal.

All investing involves risk including loss of principal. No strategy assures success or protects against loss.