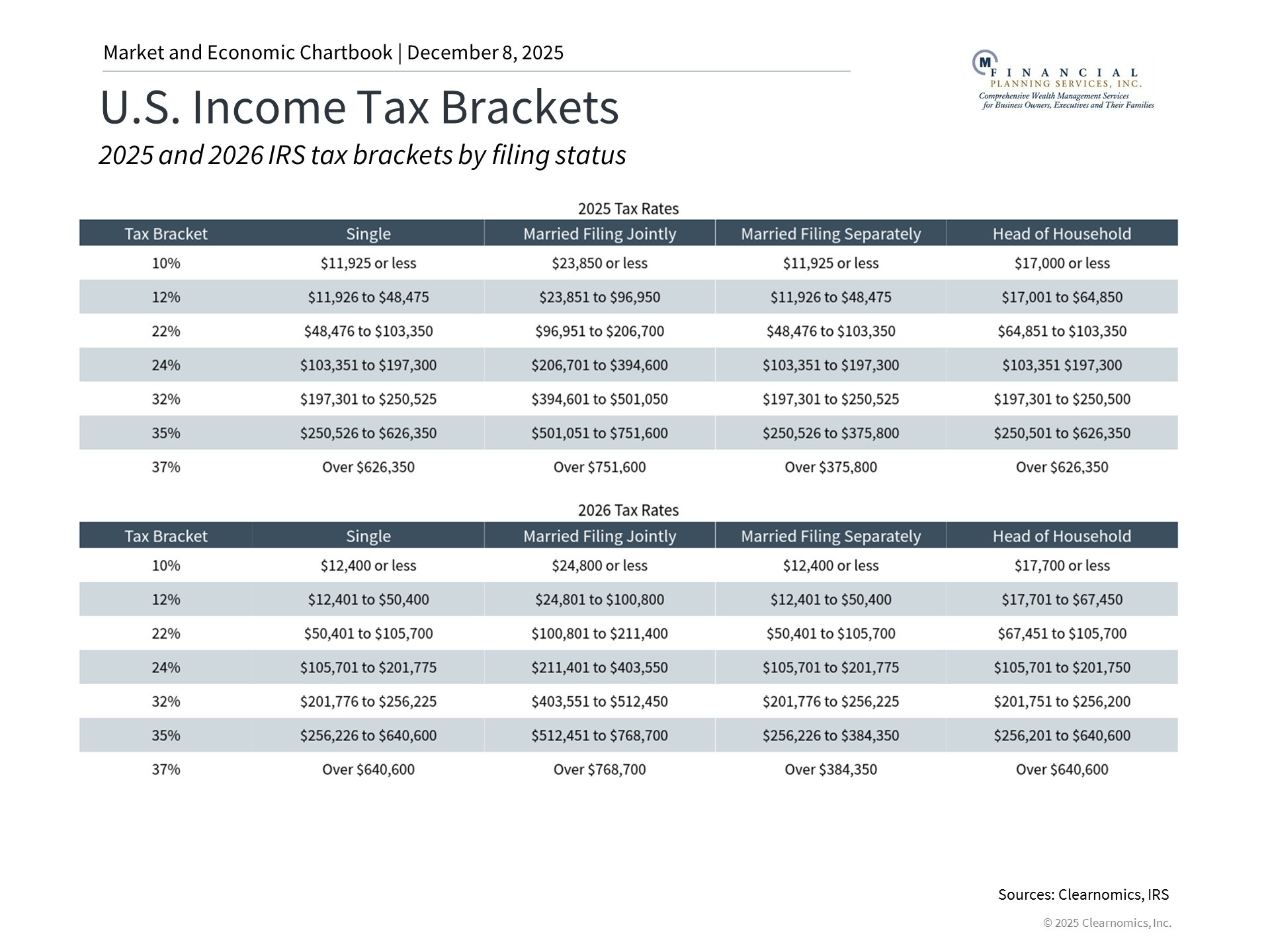

As the year comes to a close, it's time to think about some important money decisions. These choices could affect your taxes and your long-term financial health. While you should think about your finances all year, many tax deadlines fall on December 31. This makes the last few weeks of the year a good time to review your tax plans.

Here are three key areas to consider: taking money from retirement accounts, converting to Roth accounts, and setting up your investments to save on taxes. These topics can get complicated, so it's smart to talk to a professional advisor.

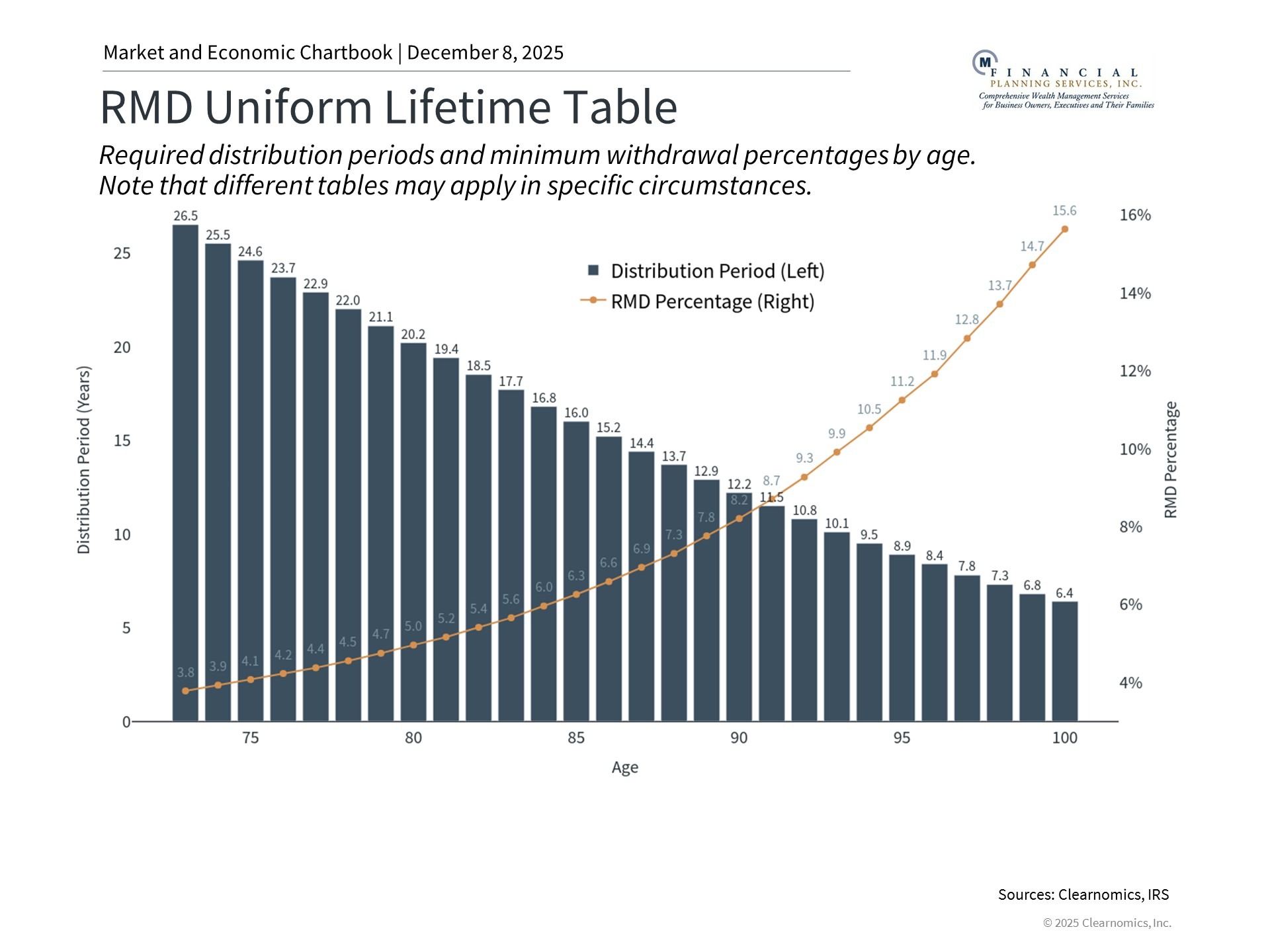

You must take required withdrawals from retirement accounts by December 31

For most of your life, you focus on saving money. But how you take money out of your retirement accounts matters just as much. This is especially true once you reach the age when you must start taking money out. Missing the December 31 deadline can cost you a lot—the penalty is 25% of the amount you should have withdrawn.

These required withdrawals are called Required Minimum Distributions, or RMDs. They apply to traditional IRAs, 401(k)s, and similar retirement accounts. You must start taking RMDs at age 73 if you turned 72 after December 31, 2022. This age will increase to 75 in 2033.

The chart shows how much you need to withdraw each year, based on your age. The amount is calculated using your account balance from the previous December 31. While the math is simple, the planning can be complex. For example, you need to decide which accounts to use first and when to take the money out during the year. The order matters because it can change how much tax you pay.

One helpful option is called a Qualified Charitable Distribution, or QCD. This lets you donate directly from your IRA to charity. The donation counts toward your required withdrawal, but you don't pay tax on it. However, timing is important with these decisions.

Converting to a Roth account can save you taxes later

Another year-end strategy is converting money from a traditional IRA to a Roth IRA. This must also be done by December 31. With this move, you pay taxes now on the money you convert. In return, the money grows tax-free, and you won't pay taxes when you take it out later.

Unlike regular Roth contributions, which have income limits, anyone can do a conversion regardless of how much they earn. Current tax rates might be lower than what you'll face in the future, which makes this strategy attractive for some people.

When deciding whether to convert, think about these factors: Compare your tax rate now to what it might be in retirement. If you expect to be in a higher tax bracket later, paying taxes now at a lower rate can save you money. Also, the longer your money can grow tax-free in the Roth account, the more valuable the conversion becomes.

Selling losing investments can reduce your tax bill

Tax-loss harvesting is a strategy for regular investment accounts (not retirement accounts). It involves selling investments that have lost value. These losses can offset any gains you made from selling other investments during the year. This must be done by December 31 to count for the current tax year.

Here's how it works: If you sold investments in 2025 and made money, you can sell other investments that lost money to offset those gains. Even if you don't have gains, you can use up to $3,000 of losses to reduce your regular income each year.

One rule to know: You can't buy back the same investment within 30 days before or after you sell it. This is called the "wash sale" rule. However, you can buy a similar investment, like a different fund that invests in the same types of things.

These strategies work best when used together

The real value comes from combining these strategies in a way that makes sense for your situation. While saving on this year's taxes is good, don't lose sight of your bigger financial goals. The best approach considers both immediate tax savings and long-term wealth growth.

The bottom line? There are several actions you can take before December 31 to help with your taxes. Now is a good time to review your situation and consider these options.

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

A Roth IRA conversion—sometimes called a backdoor Roth strategy—is a way to contribute to a Roth IRA when income exceeds standard limits. The converted amount is treated as taxable income and may affect your tax bracket. Federal, state, and local taxes may apply. If you’re required to take a minimum distribution in the year of conversion, it must be completed before converting.

To qualify for tax-free withdrawals, you must generally be age 59½ and hold the converted funds in the Roth IRA for at least five years. Each conversion has its own five-year period, and early withdrawals may be subject to a 10% penalty unless an exception applies. Income limits still apply for future direct Roth IRA contributions.

This material is for informational purposes only and does not constitute tax, legal, or investment advice. Please consult a qualified tax professional regarding your individual circumstances.